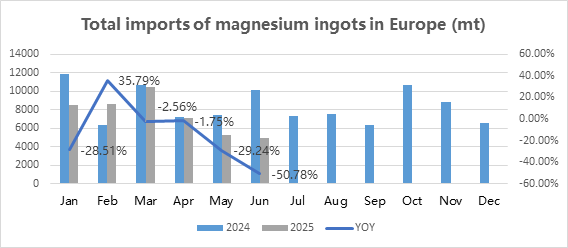

According to the latest customs import and export data, in June, magnesium ingot exports totalled 20,393 tonnes, a year-on-year decrease of 9.63%. Of this total, exports to European countries amounted to 4,972 tonnes, a year-on-year decrease of 50.78%. Looking at cumulative exports for the first half of the year, exports to Europe totalled 44,849 tonnes in the first half of 2025, a year-on-year decrease of 16.38%. Therefore, the data indicates a significant decline in Europe's demand for magnesium ingots.

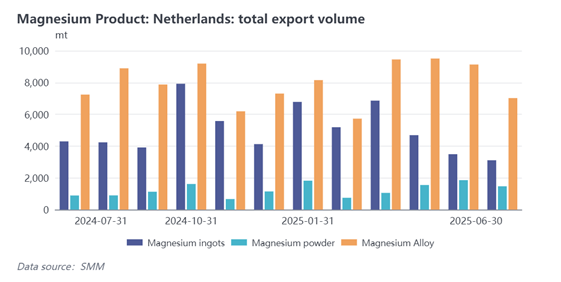

Regarding the demand for other magnesium products (magnesium powder and magnesium alloys), taking the data from the Netherlands, Europe's largest trade port, as an example, the cumulative export volume of magnesium products (magnesium ingots, magnesium alloys, and magnesium powder) to the Netherlands in the first half of 2025 was 87,627 tonnes, a decrease of 9.21% year-on-year. Specifically: magnesium ingot exports decreased by 23.36%, magnesium powder decreased by 0.89%, and magnesium alloys increased by 0.75%. This indicates that the decline in European market demand is primarily concentrated in magnesium ingot products, while demand for processed products such as magnesium powder and magnesium alloys has not experienced significant fluctuations.

From the perspective of different market participants——

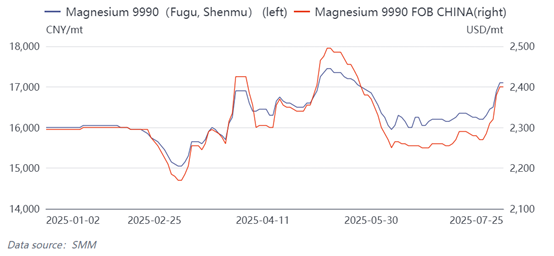

Magnesium ingot exporters report that, magnesium prices have fluctuated frequently this year, particularly with significant price differentials in FOB China prices, leading to intense price competition among traders. European customers have shifted to a ‘bid-winning’ order placement model, with some orders even resulting in losses, severely compressing profit margins. Additionally, European customers are exerting severe price pressure, partly due to downstream bearish expectations and partly because they have expanded their quotation scope, always finding quotes that meet their psychological price expectations. Traders generally note that European order volumes have indeed decreased, even from long-term customers, and many low-price orders cannot be accepted, leaving them in a passive position between magnesium plants and downstream buyers.

Magnesium ingot manufacturers believe that, their pricing is more dependent on raw material costs and domestic and international order demand. From the perspective of export orders, they argue that European customers have merely changed their procurement model: shifting from previous large-volume, concentrated purchases to multiple batches of small-volume, high-frequency orders, while expanding the scope of their inquiries. As a result, individual traders receive fewer orders, but the total volume aggregated at the manufacturer level remains stable. Additionally, manufacturers are more focused on the robust domestic market demand and do not perceive significant changes in European market demand.

European end users (including large aluminium plants, car manufacturers, and traders) clearly indicate that demand is indeed weak, and this trend may continue into the fourth quarter. There are two main reasons for this: first, technological development has stalled, with European magnesium alloy research and development progressing slowly post-pandemic, coupled with the need for a 1-2 year research period for ESG projects and insufficient personnel allocation, leading to a slow recovery in market demand; second, European automakers have been severely impacted by tariff policies this year, with weak demand in the first half of the year and slow resumption of production after the summer break, which will further drag down fourth-quarter demand. They believe that European market demand capacity remains intact, but its growth pace lags far behind Chinese. Chinese rapid advancements in lightweighting technology and production processes have made European market demand appear relatively weak in comparison.

At the policy level, the Sixth Meeting of the Central Financial and Economic Affairs Commission in July 2025 explicitly emphasized curbing 'involution' (referring to cutthroat, zero-sum competition that erodes industry-wide profitability) as the central tenet of 'Supply-Side Reform 2.0.' This policy orientation holds particular relevance for the magnesium ingot market—while price volatility requires monitoring, the priority should shift toward addressing underlying demand dynamics.

For producers, meaningful price adjustments must correlate with tangible quality enhancements, achieved through upgraded raw materials and refined production techniques to deliver specification-compliant products, thereby promoting sustainable competition. For traders, the State Taxation Administration's crackdown on 'fictitious export transactions' (a practice where companies fabricate export records to claim tax rebates illegally), effective October 1st, will rigorously standardize market operations. The current demand contraction and procurement restructuring stem primarily from export market irregularities, underscoring the urgency to implement a transparent, unified pricing framework—rather than attributing price suppression solely to weakened European demand.

SMM will continue to monitor export market order signing trends in the second half of the year, tracking real-time market price movements and market conditions.